Fiat-Collateralized Stablecoins: The Pillars of Digital Stability

Fiat-collateralized stablecoins, exemplified by USDC and USDT, are digital assets designed to maintain a 1:1 value peg to traditional fiat currencies, predominantly the US dollar. They achieve this stability by backing their circulating supply with reserves held in conventional financial institutions, acting as a crucial bridge between traditional finance and the crypto economy while introducing specific counterparty and regulatory considerations.

Key Takeaways

- **Core Mechanics & Pegging:** Fiat-collateralized stablecoins maintain a 1:1 peg to a specific fiat currency (most often USD) by holding equivalent reserves of that currency or highly liquid cash equivalents in traditional bank accounts.

- **Centralized Issuance & Associated Risks:** Operating on a 'mint-and-burn' model via a centralized issuer, these stablecoins are subject to counterparty, custodial, and operational risks, as evidenced by events like the temporary USDC de-pegging during the Silicon Valley Bank collapse.

- **Market Dominance & Diverse Use Cases:** Representing the largest category by market capitalization, these stablecoins are fundamental across crypto, enabling cross-border payments, liquidity management in DeFi, acting as a 'safe harbor' during volatility, and serving as collateral.

- **Transparency & Regulatory Scrutiny:** The quality and transparency of reserves (via attestations or audits) are critical. The evolving regulatory landscape (e.g., MiCA, Payment Stablecoin Act) aims to enforce reserve segregation, redemption rights, and capital buffers to mitigate systemic risks.

- **USDC vs. USDT:** While both are leading fiat-collateralized stablecoins, they differ significantly in their regulatory approaches, reserve transparency, and market focus, influencing institutional adoption and developer integration choices.

Fiat-Collateralized Stablecoins: The Pillars of Digital Stability

Introduction

Fiat-collateralized stablecoins represent a dominant category of digital assets engineered to maintain a 1:1 peg to a specific fiat currency, most commonly the US dollar. Their value is directly derived from reserves held in traditional financial institutions, providing a vital anchor of stability within the inherently volatile cryptocurrency market. These stablecoins play a pivotal role in the broader digital asset ecosystem, underscored by their significant market capitalization, which consistently surpasses other stablecoin categories. Two preeminent examples are USD Coin (USDC) and Tether (USDT), which together have historically commanded a combined market significance exceeding $100 billion in circulating supply. This article will thoroughly explore their core mechanics, reserve composition, issuance models, the intricate regulatory landscape, inherent risks, and diverse use cases across professional domains.

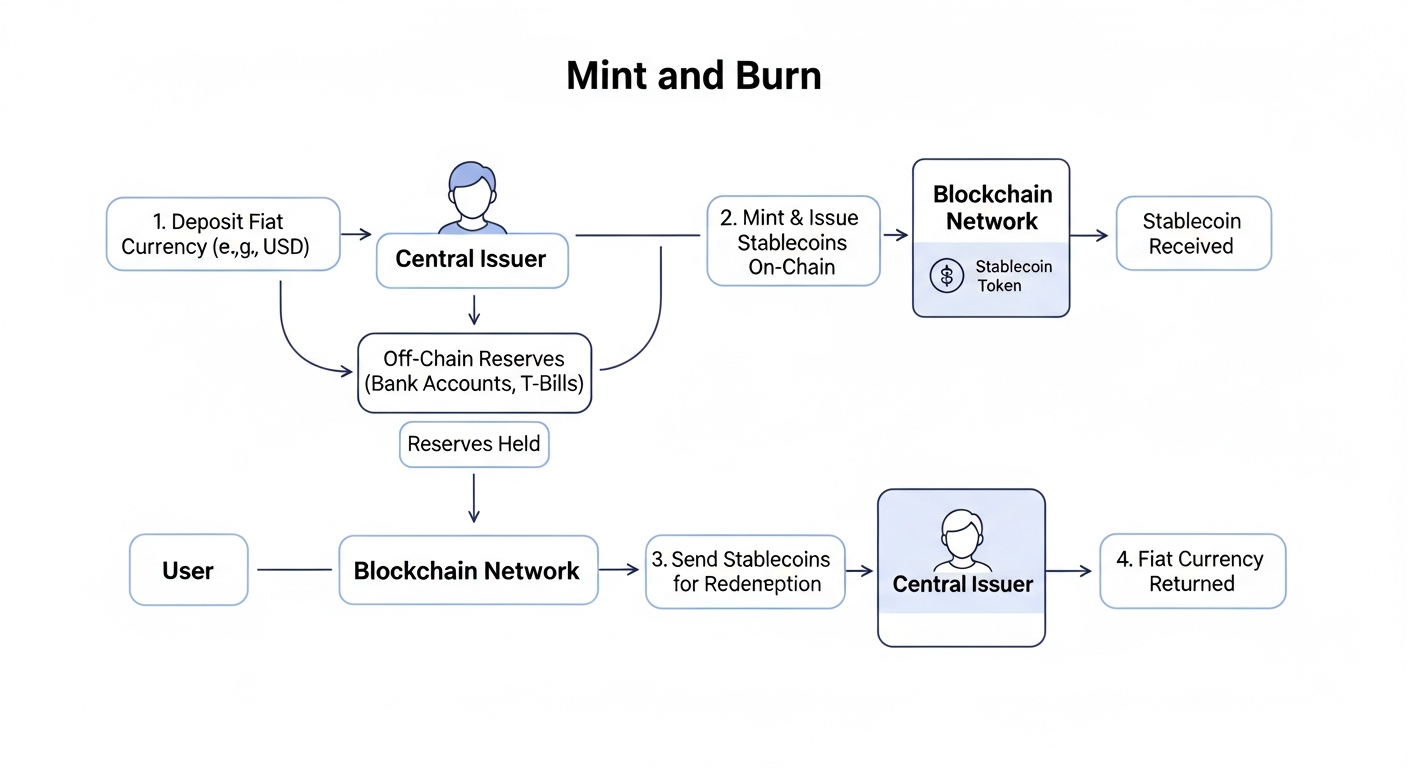

How Fiat-Collateralized Stablecoins Work: Core Mechanics

Fiat-collateralized stablecoins primarily operate on a 'mint-and-burn' issuance model. The process begins when a user deposits fiat currency with a central issuer. In exchange, the issuer creates (mints) an equivalent amount of tokens on a blockchain, delivering them to the user. Conversely, these tokens can be redeemed for fiat currency at any time, ensuring robust liquidity and price stability. The custodial infrastructure supporting these stablecoins involves reserves held in highly liquid and secure instruments, such as segregated bank accounts, money market funds, short-duration Treasury bills, and other cash-equivalent instruments. Central issuers serve as trusted intermediaries, critically tasked with meticulously maintaining the peg, diligently managing the reserve assets, and efficiently processing all redemption requests. This clear distinction between on-chain token supply and off-chain reserve holdings, while streamlining operational efficiency, inherently introduces counterparty risk due to the reliance on the issuer's solvency and integrity.

Reserve Composition and Attestation

The precise composition of reserves can vary significantly among issuers, reflecting different risk appetites and regulatory approaches. For instance, Tether (USDT) has historically diversified its holdings to include commercial paper, secured loans, and other assets, whereas USD Coin (USDC) typically adopts a more conservative strategy, focusing predominantly on cash and short-term US Treasuries. Issuers routinely provide monthly or quarterly attestation reports from independent third-party accounting firms. While these attestations offer a valuable snapshot of reserve holdings at a specific point in time, they differ from full GAAP-compliant audits, which would provide a deeper, more comprehensive level of assurance to creditors, token holders, and regulators regarding the issuer's financial health and controls. Transparency in reserve holdings is paramount for fostering institutional adoption, facilitating robust counterparty due diligence, and accurately assessing systemic risk. A key aspect of the issuer's business model is generating revenue by investing these reserves in interest-bearing instruments, thereby benefiting from the reserve yield, while token holders typically do not receive a direct yield on their stablecoin holdings.

Key Market Participants and Use Cases

Fiat-collateralized stablecoins serve a broad spectrum of market participants and facilitate numerous critical use cases:

- Financial Professionals and Institutions: Leverage stablecoins for efficient cross-border settlements, optimizing intraday liquidity management, and as a stable medium of exchange within decentralized finance (DeFi) protocols.

- Developers and Builders: Integrate USDC and USDT into innovative payment systems, cost-effective remittance applications, decentralized exchanges (DEXs), and lending protocols, benefiting from their deep liquidity and multi-chain availability.

- Investors and Market Analysts: Utilize stablecoins as a 'safe harbor' asset during periods of extreme crypto market volatility, for executing sophisticated arbitrage strategies, and as collateral in margin trading and various yield-generating protocols.

- Regulators and Policymakers: Recognize fiat-collateralized stablecoins as the most systemically significant category due to their immense scale, global cross-border reach, and potential implications for monetary policy transmission and financial stability.

Risks and Vulnerabilities

Despite their substantial advantages, fiat-collateralized stablecoins are not without significant risks:

- Custodial and Counterparty Risk: This arises from the issuer's solvency, operational integrity, and banking relationships. A prominent example is the temporary de-pegging of USDC in March 2023 following the collapse of Silicon Valley Bank, where a portion of its reserves were held.

- Concentration and Operational Risk: Reliance on a single, centralized issuer introduces vulnerabilities such as potential blacklisting of addresses, freezing of accounts, and susceptibility to unilateral regulatory or legal actions.

- Reserve Quality Risk: Concerns emerge when reserves consist of illiquid, risky, or credit-impaired assets. Such a composition could lead to forced asset fire sales during periods of high redemption demand, potentially disrupting the stablecoin's peg.

- Regulatory and Legal Risks: These are prevalent due to ongoing jurisdictional uncertainties, the potential classification of stablecoins as securities, and evolving Anti-Money Laundering (AML) and Know Your Customer (KYC) compliance requirements.

Regulatory Landscape and Policy Implications

The global regulatory landscape for fiat-collateralized stablecoins is rapidly evolving. In the United States, proposed legislation like the Payment Stablecoin Act aims to establish a comprehensive framework. Concurrently, the European Union's landmark MiCA (Markets in Crypto-Assets) regulation mandates explicit reserve requirements, licensing for issuers, and robust governance for 'asset-referenced tokens.' Other leading financial jurisdictions, including the UK, Singapore, and Hong Kong, are also actively formulating their respective regulatory frameworks. Key regulatory requirements frequently include mandatory reserve segregation, regular public attestations or full audits, explicit redemption rights for token holders, and adequate capital buffers for issuers. The systemic risk debate continues to center on whether large-scale stablecoins could potentially disintermediate traditional banks, affect the efficacy of central bank monetary policy, or introduce new forms of financial instability. Comparisons with Central Bank Digital Currencies (CBDCs) often highlight the strategic positioning of private-sector stablecoins as either complementary or competitive forces to state-backed digital currencies.

USDC vs. USDT: A Comparative Perspective

| Feature | USD Coin (USDC) | Tether (USDT) |

|---|---|---|

| Issuer | Circle (US-regulated fintech) | Tether Holdings Limited (British Virgin Islands) |

| Regulatory Stance | Emphasizes institutional compliance and US regulatory alignment | Historically faced greater scrutiny regarding transparency and regulatory compliance |

| Reserve Transparency | Higher; monthly attestations from Deloitte, focused on cash/short-term US Treasuries | Historically less transparent; settled with CFTC in 2021 over reserve disclosures |

| Market Cap & Trading | Strong in institutional and DeFi integration, growing market share | Largest market cap, dominant in offshore trading pairs and crypto-to-crypto liquidity |

| Blockchain Availability | Multi-chain (Ethereum, Solana, Avalanche, etc.) | Multi-chain (Ethereum, Tron, Solana, etc.) |

| Smart Contracts | Well-audited, often seen as 'blue-chip' for integrations | Extensive usage, but some perceive higher centralization risks due to historical practices |

Strategic Considerations for Professionals

- For Financial Institutions: Thoroughly evaluating an issuer's creditworthiness, the precise composition and liquidity of its reserves, and the clarity of its redemption terms is paramount before integrating stablecoins into operational frameworks.

- For Developers: Assessing smart contract audit history, understanding the issuer's blacklisting capabilities, and scrutinizing the security and reliability of cross-chain bridge mechanisms are critical for robust integration.

- For Investors: Continuously monitoring reserve disclosures, keeping abreast of relevant regulatory developments, and analyzing on-chain metrics are essential for gauging peg stability and making informed investment decisions.

- For Regulators: Developing comprehensive frameworks that enforce stringent reserve quality standards, mandate real-time public disclosure, and promote interoperability will be key to balancing innovation with financial stability and consumer protection.

Conclusion

Fiat-collateralized stablecoins deliver compelling benefits of simplicity, robust liquidity, and price stability, all anchored to familiar traditional fiat systems. Their inherently centralized structure offers advantages in terms of regulatory legibility and established trust mechanisms but concurrently introduces specific counterparty, custodial, and censorship risks. The dynamic and evolving global regulatory environment will undoubtedly play a significant role in shaping the future competitive landscape among established players like USDC and USDT, as well as emergent, compliant alternatives. Readers are encouraged to further explore related topics such as algorithmic stablecoins, crypto-collateralized models, and Central Bank Digital Currencies (CBDCs) for a holistic and comprehensive understanding of the rapidly evolving digital money landscape.

Comments

Sign in to join the discussion

Sign In to Comment