Beyond the Tap: Deconstructing Digital Payments from Clearing to Settlement

Every digital payment initiates a complex, multi-stage process distinguishing instant information flow from the slower, risk-managed movement of actual value. Understanding this architecture, encompassing clearing, settlement, and the roles of various financial entities, is crucial for comprehending how money truly moves in the modern economy.

Key Takeaways

- Digital payments involve a fundamental separation: payment *information* (e.g., authorization) travels almost instantly, while the actual *value* (funds) moves later, often due to risk management, netting efficiency, and batch processing.

- Clearing is the process of validating, matching, and netting obligations between parties, often through a clearing house. Settlement is the final, irrevocable transfer of funds, typically using central bank money, with Real-Time Gross Settlement (RTGS) offering immediate finality and Deferred Net Settlement (DNS) offering batched finality.

- The global payment landscape is diverse, comprising systems like Fedwire (US RTGS), ACH (US batch retail), T2 (Eurozone RTGS), and SEPA (European retail), each balancing speed, cost, finality, and risk. Cross-border payments, primarily via correspondent banking and SWIFT messaging, face unique challenges like multi-day settlement and high fees.

- Banks are central, acting as intermediaries, managing accounts, and holding deposits. Payment Service Providers (PSPs) and Electronic Money Institutions (EMIs) facilitate payments but do not operate with fractional reserves like traditional banks, typically moving money rather than creating it.

- Payment security and authentication differ significantly between proximity (in-person) and online (card-not-present) transactions, with online payments requiring more robust authentication layers (e.g., 3D Secure, SCA) to mitigate higher fraud risks, despite using the same underlying clearing and settlement rails.

Introduction: The Invisible Architecture of Money Movement

Every digital payment triggers a complex chain of events invisible to the end user—from a tap of a card to a wire transfer settling billions. When you make a payment, there's a fundamental distinction between the movement of payment information and the actual movement of value — a critical distinction most people overlook.

At the heart of every payment system are two core stages: clearing and settlement. Understanding this infrastructure is crucial for financial professionals, regulators, and anyone building or overseeing modern payment systems. It provides insight into how payments are processed, the risks involved, and how innovations can integrate or disrupt existing frameworks.

Information Flow vs. Value Flow: Two Separate Journeys

Payment information, consisting of instructions, authorizations, and messages, travels almost instantly across networks. However, the actual movement of value does not occur at the same speed. For instance, when you tap your card at a store, an authorization message is sent and approved within seconds, but the actual funds may not be transferred and settled between the banks involved until hours or even days later.

A 'payment message' is essentially a signal or an instruction, while a 'fund transfer' is a definitive ledger adjustment between financial institutions. This separation exists due to critical reasons: it allows for robust risk management, enables netting efficiency (reducing the total value needing to be exchanged), and reflects the batch processing heritage of banking infrastructure.

Clearing: Sorting, Verifying, and Netting

Clearing is the initial process of reconciling orders between transacting parties — validating, matching, and calculating net obligations. Its primary function is to prepare transactions for settlement. Through multilateral netting, clearing houses aggregate numerous payment obligations among multiple participants so that only net amounts need to settle, rather than settling every transaction individually. For example, if Bank A owes Bank B $100 and Bank B owes Bank A $80, netting ensures only Bank A settles a net $20 to Bank B.

Central Counterparties (CCPs) and clearing houses play a crucial role in absorbing and managing counterparty risk by acting as the buyer to every seller and seller to every buyer. Clearing can occur in batches at the end of the day (e.g., for retail payments) or continuously throughout the day, depending on the system and the type of payment.

Settlement: When Value Actually Moves

Settlement is the final, irrevocable transfer of funds between financial institutions, marking the moment obligations are discharged. This is when ownership of the underlying assets (money) legally and operationally changes hands. There are two main types of settlement:

- Deferred Net Settlement (DNS): This involves batching transactions throughout the day, calculating the net obligations, and settling these net amounts at a specified time, typically at the end of the day. It offers end-of-day finality and is common for retail payment systems due to its cost efficiency.

- Real-Time Gross Settlement (RTGS): In an RTGS system, each transaction settles individually and immediately upon processing, providing immediate and irrevocable finality. This system is primarily used for large-value, time-critical interbank payments, where the immediate finality significantly reduces systemic risk.

Settlement finality is crucial both legally and operationally, as it ensures a payment cannot be reversed after settlement, thereby providing certainty to all parties. Central bank money, held in accounts at the central bank, is often the ultimate settlement asset, as it carries no credit risk. Most large-value interbank payments settle across these central bank accounts. Settlement risk arises when a participant cannot meet its net obligation (in DNS) or fund its gross obligations (in RTGS) due to liquidity issues at the time of settlement.

Card Payments: Visa and Mastercard Networks in Action

Visa and Mastercard are not banks but rather network operators and messaging infrastructure providers. Crucially, they do not hold customer funds; instead, they facilitate the communication and data exchange between financial institutions. A card payment lifecycle starts when a cardholder initiates a payment at a merchant. The merchant's acquiring bank (or 'acquirer') sends an authorization request through the card network (e.g., VisaNet or Mastercard's Banknet) to the cardholder's issuing bank ('issuer'), which returns an approval or decline.

This is known as the four-party model, involving the cardholder, the merchant, the acquiring bank, the card network, and the issuing bank. Each player is essential. Proximity payments, such as contactless (NFC) or chip-and-PIN transactions, involve in-person interactions where the card or device is physically present. Online payments (often referred to as 'card-not-present' transactions) involve different fraud risks and require more robust authentication requirements. Interchange fees, paid by the acquiring bank to the issuing bank, are a key component of how value is allocated among the parties in the card payment ecosystem. Card transactions clear and settle separately from the initial authorization process, with VisaNet and Mastercard's Banknet handling the clearing of transaction data, while the actual fund settlement typically occurs via designated settlement banks or central bank accounts.

Domestic Payment Systems: Fedwire and European Infrastructure

In the US, the Fedwire Funds Service is a Real-Time Gross Settlement (RTGS) system used for large-value, same-day final settlement between US depository institutions. It is essential for time-critical interbank transfers, such as large corporate payments, bank-to-bank funding, and capital market transactions, providing immediate finality and reducing systemic risk. In contrast, the Automated Clearing House (ACH) system handles batch retail payments like payroll direct deposits, bill payments, and person-to-person transfers. ACH offers lower transaction costs but typically involves delayed finality, with funds settling within one to three business days.

In Europe, T2 (which replaced TARGET2) is the European Central Bank's RTGS system for euro-denominated large-value payments across the Eurozone. It functions similarly to Fedwire, ensuring immediate and final settlement for critical transactions. The Single Euro Payments Area (SEPA) simplifies retail payments, enabling euro credit transfers and direct debits across 36 European countries under a uniform set of rules, making cross-border euro payments as easy as domestic ones. SEPA Instant Credit Transfer (SCT Inst) further enhances this by providing real-time retail payment capabilities, with clearing and settlement finality typically achieved within 10 seconds, 24/7/365. These domestic systems reflect each jurisdiction's balance between speed, finality, risk, access, and cost efficiency.

Cross-Border Payments: SWIFT and the Correspondent Banking Network

SWIFT, the Society for Worldwide Interbank Financial Telecommunication, is a global, secure messaging network that moves standardized payment instructions between financial institutions, not the money itself. Cross-border payments overwhelmingly rely on the correspondent banking network, which involves a complex chain of bilateral relationships between banks in different countries. Each bank typically holds nostro/vostro accounts with their correspondent partners, pre-funding accounts in foreign currencies to facilitate transactions.

For example, a payment initiated by a customer at a bank in Brazil to a recipient at a bank in Japan may pass through several intermediary correspondent banks (e.g., in New York or London) before reaching its final destination. Key challenges of this traditional system include multi-day settlement times, high fees (due to multiple intermediaries), limited transparency regarding the payment's status and final costs, and trapped liquidity in pre-funded accounts. To address some of these frictions, SWIFT introduced SWIFT gpi (Global Payments Innovation), an upgrade layer that offers tracking capabilities, speed commitments, and fee transparency. Beyond SWIFT, alternatives are emerging to address cross-border friction, such as multilateral payment platform initiatives and linked fast payment systems between countries, aiming to increase speed and reduce costs.

The Role of Banks in the Payment System

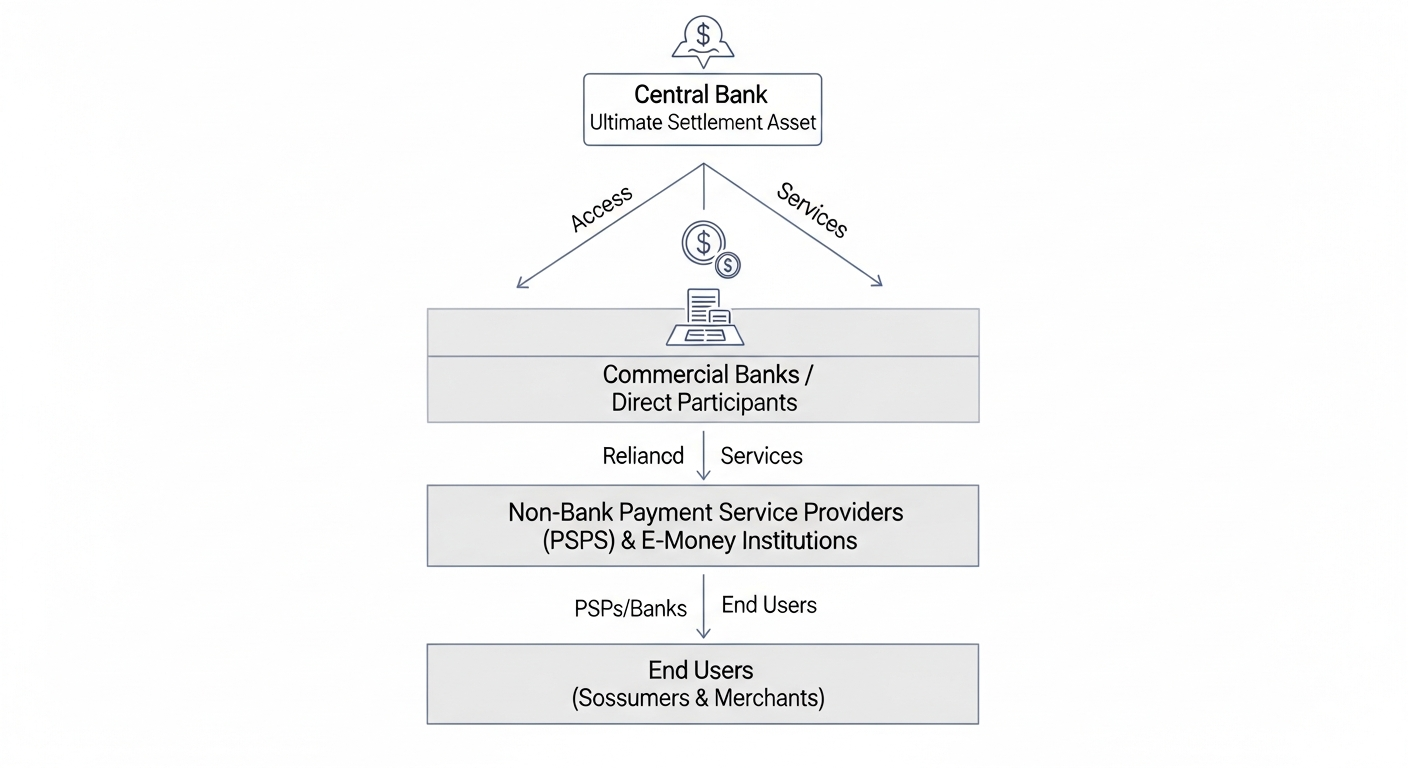

Banks perform multiple, interconnected roles within the payment system. They hold customer deposits, extend credit, operate payment accounts, and act as crucial intermediaries in the clearing and settlement chains. The structure of payment systems is often tiered: central banks sit at the top, providing the ultimate settlement asset (central bank money). Commercial banks with direct access to central bank accounts and payment systems are considered Tier 1 participants. Smaller banks, credit unions, and many fintechs (Tier 2 participants) typically access these systems indirectly through a sponsor bank, leveraging the sponsor's direct access.

Banks also manage intraday liquidity by using central bank credit or pledging collateral to fund their payment obligations throughout the day, ensuring they can meet their commitments before net settlement occurs. As key participants in this infrastructure, banks bear significant operational, credit (the risk that a counterparty defaults), and liquidity risk (the risk of not having enough funds to meet obligations) inherent in the processing and settlement of payments.

Payment System Providers and Electronic Money Institutions

Payment Service Providers (PSPs), such as PayPal, Stripe, and Adyen, differ from traditional banks. While they facilitate payments, they typically do not create money through fractional reserve banking; rather, they move existing money between accounts. They serve as technological and operational intermediaries, often aggregating services across multiple payment methods and networks.

Electronic Money (e-money) is a digital store of value issued by a licensed e-money institution (EMI). It is backed 1:1 by fiat currency held in segregated, safeguarded accounts, meaning it is not a bank deposit and thus not typically covered by deposit guarantee schemes. EMIs access underlying payment rails—whether card networks, bank payment schemes, or SWIFT—through either a sponsored connection via a bank or, in some jurisdictions, direct access. Unlike banks, EMIs are legally prohibited from lending customer funds and must safeguard customer balances, making them structurally distinct from fractional-reserve banks. Beyond EMIs, Payment Aggregators and payment orchestration layers play a vital role in routing transactions across multiple networks for optimization, cost efficiency, and improved success rates.

Proximity vs. Online Payments: Same Rails, Different Risk Profiles

Proximity payments occur in-person, typically using technologies like contactless NFC (Near Field Communication) for tap-to-pay or EMV chip-and-PIN transactions. In these scenarios, the card or payment device is physically present, and authentication often happens directly at the point-of-sale terminal (e.g., via PIN, fingerprint, or device unlock). This physical presence and on-device authentication generally reduce the risk of fraud.

Online payments (also known as 'card-not-present' transactions) carry higher inherent fraud risks due to the lack of physical verification of the card or cardholder. Consequently, they require additional authentication layers to mitigate these risks. Examples include 3D Secure (3DS) protocols, one-time passwords (OTPs) sent to a registered mobile device, or biometric verification. Regulations like Strong Customer Authentication (SCA) under PSD2 in Europe have further enhanced online payment security by mandating two-factor authentication for most digital transactions. Crucially, both proximity and online payments ultimately use the same underlying card network clearing and settlement infrastructure; the primary differences lie in the point of initiation and the robust authentication layers applied.

Conclusion: Why This Architecture Matters

The layered and interconnected nature of payment systems—involving networks carrying messages, banks holding accounts, clearing houses netting obligations, and central banks providing final settlement—is the invisible engine of the global economy. Understanding the fundamental distinction between information and value flow forms the conceptual foundation for comprehending any payment system, whether traditional or emerging.

The resilience, inclusivity, cost-effectiveness, and speed of these payment systems directly affect economic participation, financial stability, and global commerce. A deep understanding of this foundation is essential context for evaluating any innovation—whether stablecoins, instant payment schemes, or new cross-border frameworks—against the existing infrastructure they must integrate with, complement, or potentially replace. This architectural insight empowers professionals to build better, more secure, and more efficient financial systems for the future.

Comments

Sign in to join the discussion

Sign In to Comment